Python 做大量组合的均值方差模型

1、导入相关包和模块

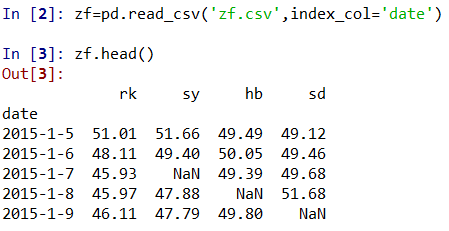

2、读取数据 zf=pd.read_csv('zf.csv',index_col='date')

并查看前5项 zf,head()

3、对缺失值的删除操作 zf=zf.dropna()

对数据的时间序列操作 zf.index=pd.to_datetime(zf.index)

4、连续收益率 zfr=np.log(zf/zf.shift(1))

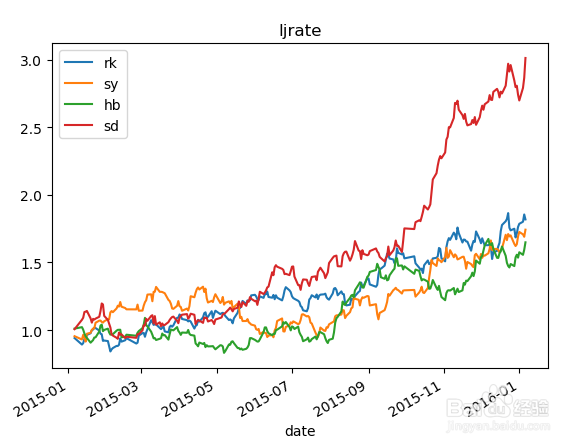

累积收益率分布图 (1+zfr).cumprod().plot(),plt.title('ljrate')

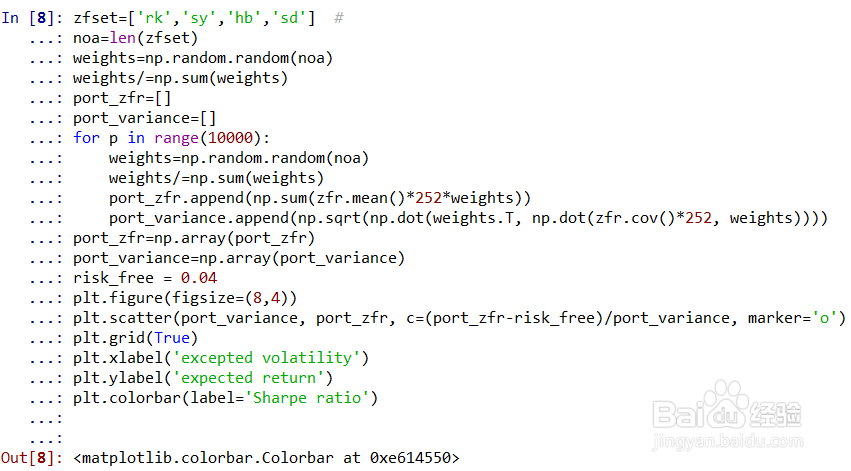

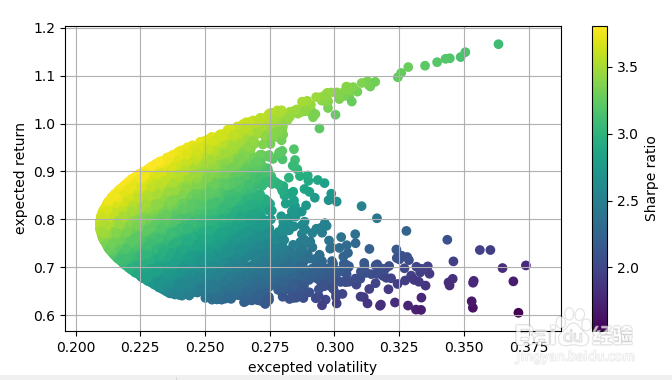

5、做大量的随机资金权重相应的收益率与方差值

zfset=['rk','sy','hb','sd']

noa=len(zfset)

weights=np.random.random(noa)

weights/=np.sum(weights)

port_zfr=[]

port_variance=[]

for p in range(10000):

weights=np.random.random(noa)

weights/=np.sum(weights)

port_zfr.append(np.sum(zfr.mean()*252*weights))

port_variance.append(np.sqrt(np.dot(weights.T, np.dot(zfr.cov()*252, weights))))

port_zfr=np.array(port_zfr)

port_variance=np.array(port_variance)

risk_free = 0.04

plt.figure(figsize=(8,4))

plt.scatter(port_variance, port_zfr, c=(port_zfr-risk_free)/port_variance, marker='o')

plt.grid(True)

plt.xlabel('excepted volatility')

plt.ylabel('expected return')

plt.colorbar(label='Sharpe ratio')